The most interesting part of this interview is the revelation that Rakesh Jhunjhunwala did not sell his core portfolio stocks in 2008 even when he was v bearish on the markets

Categories

Linkfest: December 06,2016

Some stuff I am reading today morning:

Amma passes away (ET)

Cyrus Mistry details hurdles facing Tata Firms (Mint)

10 Year SIP Returns are less than 8% (CapitalMind)

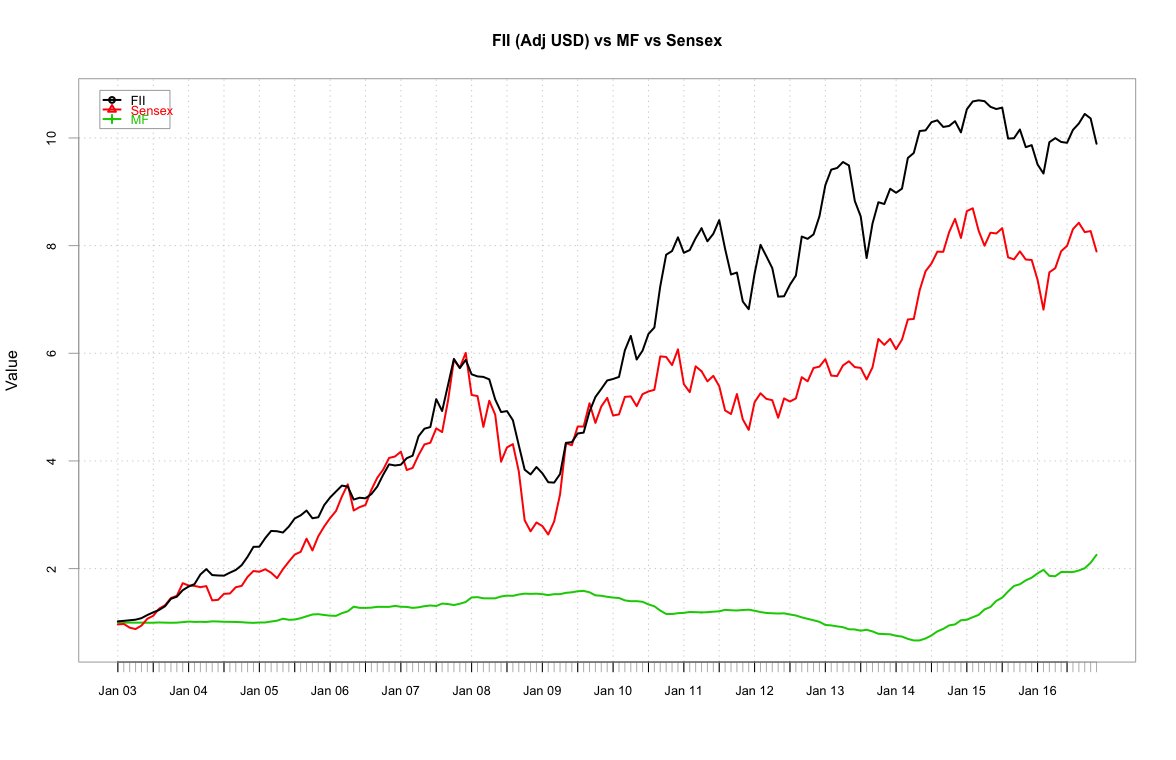

How foreign investors are viewing India (MorningStar)

Modi isn’t a diamond’s best friend (Bloomberg)

Everyone is in Sales (Common Sense)

The Permanent Portfolio (IRR)

What does it take to be a world-class investor? (Pension Partners)

A dozen things Buffett learnt from See’s Candies (25IQ)

AIB:The Demonetization Circus (YouTube)

Categories

Chart:Who moves the Sensex?FII or DII

Categories

Linkfest:December 05,2016

Some stuff I am reading today morning:

Markets braced for turmoil as ‘No’ wins Italy referendum (Telegraph)

Italian banks on the brink (DR)

Did Fairfax screw Adi Finechem’s minority shareholders? (ML)

2 Controversies that prompted Chitra’s resignation (Quint)

IPO Review:Avoid Laurus Labs (S P Tulsian)

Where do MFIs go from here? (Mint)

Stock Talk: Siyaram Silk Mills (RJ)

Buying “low” Vs Buying “systematically” (FreeFinCal)

Renegotiate the agreement value of your flat (Ravi)

Winton Capital is making Millions through Maths (Climateer)

Categories

Top Clicks on Alpha Ideas This Week

Here are the most clicked on items this week on Alpha Ideas :

Puneet Dalmia on how to play India Cement (AI)

Biyani on Retail (AI)

Porinju Veliyath’s top 10 picks (RJ)

Quality Dividend Yield Stocks (AI)

Here’s what Modi may do next (Forbes)

Analysis: Indo Count Industries (Dr.Vijay Malik)

Demonetization as I see it (Ambareesh Baliga)

Jets loaded with cash draw India’s ire (Bloomberg)

When FIIs sell (AI)

India’s demonetization could be the first cash domino to fall (Forbes)