Hat tip: Sunil Singhania

Hat tip: Sunil Singhania

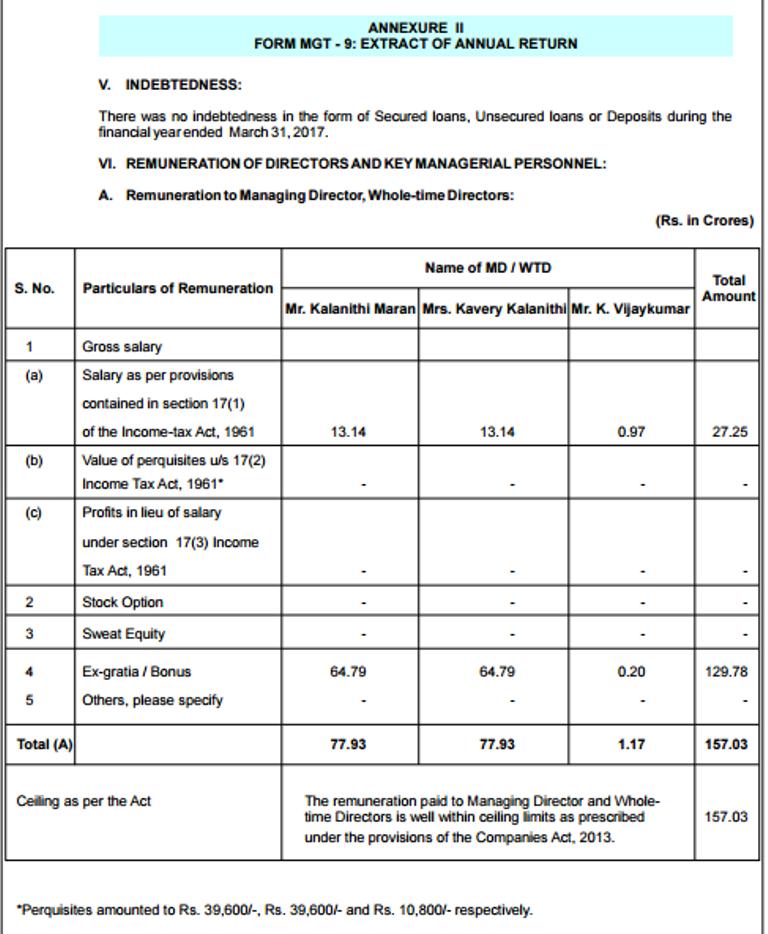

Source: Sun TV Annual Report

Amount spent by Sun TV on CSR

Amount spent by Sun TV on the salaries of the Promoter and his wife:

SHAME, SHAME !!

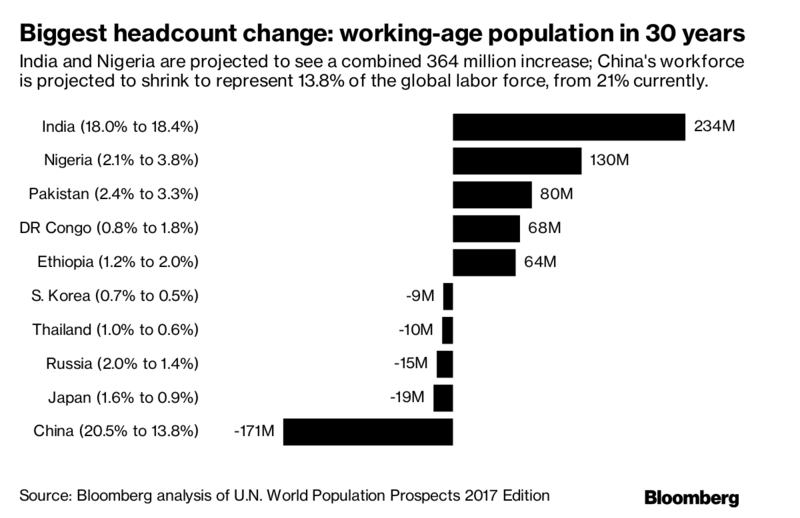

When I bought Hdfc in 1979 and 1980 there was 1 Housing finance company. Now there are 125. All expecting to grow at 30% CaGR. Lovely.

— Subramanyam PV (@pvsubramanyam) September 6, 2017

Source: Bloomberg

Some stuff I am reading today morning:

A disruptive “Patanjali Moment” awaits Indian Pharma (MC)

Accounts frozen, 2L Companies get shell shocked (ET)

IPO Analysis: Bharat Road Network (Mint)

ICICI Lombard gets SEBI approval for IPO (BL)

5 Micro Cap Stocks with Multi-Bagger Potential (Mudar Patherya)

Tiny changes can have big implications (Prof Sanjay Bakshi)

When the hedge is worse than the thing being hedged (TRB)

What I learned in the last year (Morgan Housel)

Averaging Down (Market Fox)

Hong Kong: 1300 Buyers fight over 4 Flats (SCMP)