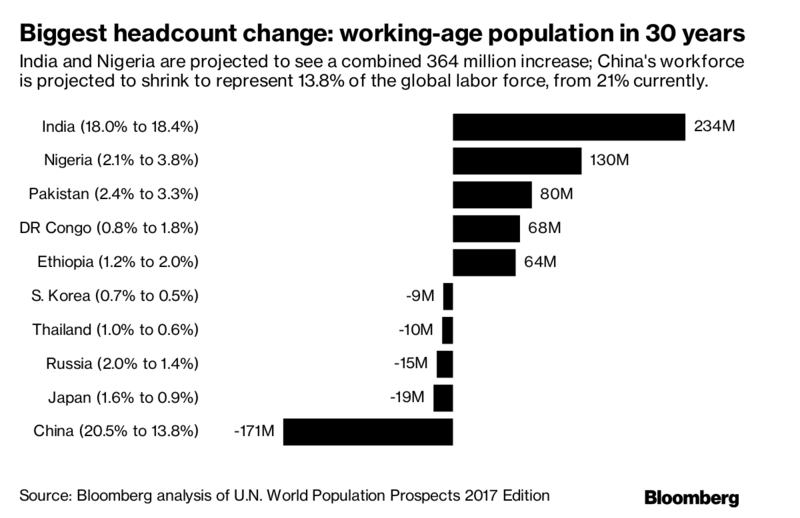

Source: Bloomberg

Source: Bloomberg

Some stuff I am reading today morning:

A disruptive “Patanjali Moment” awaits Indian Pharma (MC)

Accounts frozen, 2L Companies get shell shocked (ET)

IPO Analysis: Bharat Road Network (Mint)

ICICI Lombard gets SEBI approval for IPO (BL)

5 Micro Cap Stocks with Multi-Bagger Potential (Mudar Patherya)

Tiny changes can have big implications (Prof Sanjay Bakshi)

When the hedge is worse than the thing being hedged (TRB)

What I learned in the last year (Morgan Housel)

Averaging Down (Market Fox)

Hong Kong: 1300 Buyers fight over 4 Flats (SCMP)

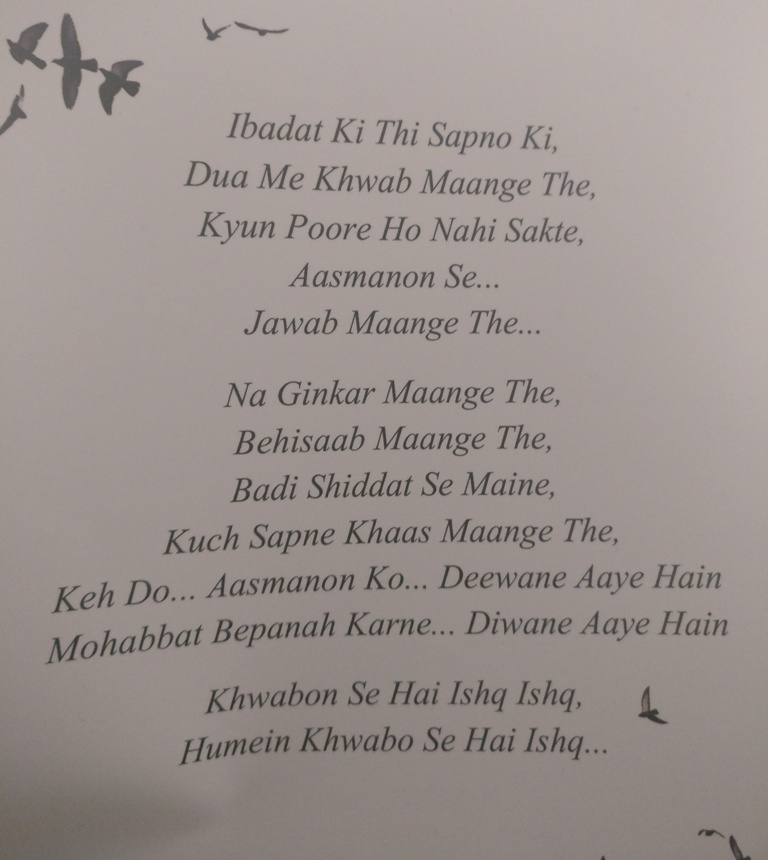

Hero Fincorp aims to be known as India’s Next-Gen Ultra Lean Credit Champion !

This poem from their Annual Report captures their ambition and determination.

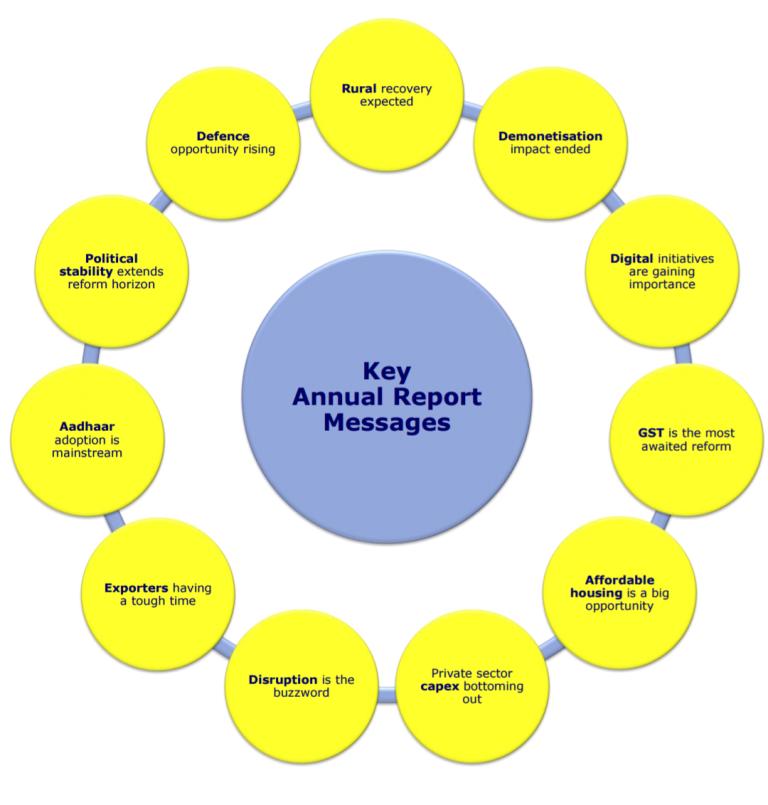

Source: CLSA Research