(Anybody wishing to buy/sell L&T Infotech shares,kindly contact me at Alpha Ideas )

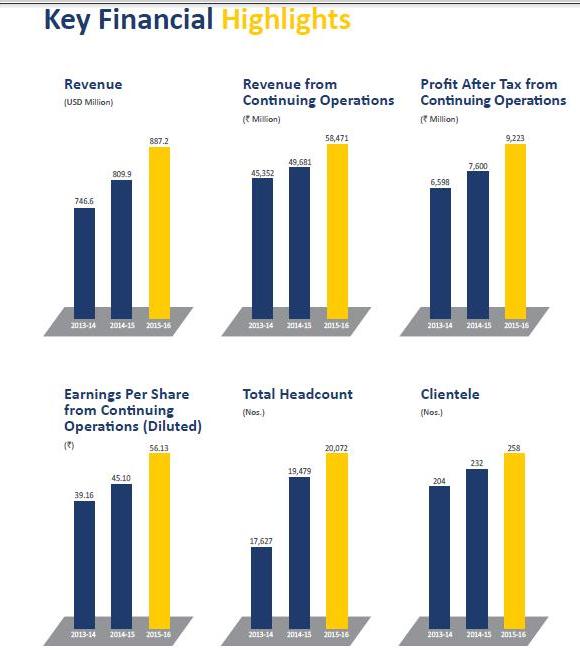

Source: L&T Infotech Annual Report 2015-16

(Anybody wishing to buy/sell L&T Infotech shares,kindly contact me at Alpha Ideas )

Source: L&T Infotech Annual Report 2015-16

China’s biggest brokerage houses are using online videos and live streams of attractive, female analysts to tout stocks—and China’s regulators don’t like it.

Some stock analysts have turned into cyber stars in China in recent days, after presenting their research online. One prominent example is Liao Lei, a stock analyst with Founder Securities, who is arguably better known for her costumes than her research.

In one clip posted Apr. 7 on video-sharing app Meipai, Liao, dressed in traditional Han Chinese robe known as Hanfu, “strongly recommends” investors buy shares in Chinese telecom firm ZTE. “Currently, the size of the company’s revenue and cash flow have reached the best level in history, and the gross margin is relatively stable,” she says to the camera, with her hand propping up her cheek.-from Quartz

CNBC India,take a bow !

But for the company itself, the most perilous years were those that followed the first world war. These years form the most interesting part of Keenan’s memoir, especially in light of Tata Steel’s current predicament. If the current glut of cheap Chinese steel has Tata haemorrhaging losses of £1m a day, in 1922, the company was brought to the brink of ruin by the flood of “cheap Continental steel smelted out of scrap from the French and Flemish battlefields”. At one point it seemed that they were not going to weather “the boatloads of Belgian steel raffled off and dumped in Calcutta and Bombay for next to nothing”. The situation became so bleak that someone suggested the colonial government be asked to take over. But the son of J. N. Tata—he had died in 1904—“pounded angrily on the table and shouted that day would never come as long as he lived”.

Fortunately, there was a plan beyond the theatrics. The company approached the government with figures to prove that it was impossible to survive against tariff-free continental steel. The government acted decisively and set up a Tariff Board to create a protective Act. It saved the day. Soon the company was back to paying shareholders a handsome dividend. All this, acknowledges Keenan, “largely because of the staying hand of a much-maligned Government.”-from Economist

Amusing to know that German shareholders share our love for AGM buffets.

As Daimler AG shareholders approved the biggest dividend in the company’s history, two investors got into a fight at its annual general meeting over complimentary sausages.

The world’s second-biggest luxury-car maker called police to calm things down after one man began packing away multiple sausages from the buffet. A woman intervened, and the two got into a verbal altercation.

Daimler served about 12,500 wursts to the 5,500 shareholders who attended the meeting in Berlin, spokeswoman Silke Walters said. Buffets that can cost far more than one share of stock are part of the culture of European shareholder meetings, which can drone on the better part of a full day as investors chow down on everything from hearty pretzels and bratwurst to coffee and cake.

Daimler shareholders approved a dividend of 3.25 euros per share on Wednesday, enough for a double-pack of sausages at German discounter Aldi. Still, Chairman Manfred Bischoff mused at the meeting, clearly the company needs to do more to satisfy their hunger.

“Either we need more sausages, or we’ll have to get rid of the sausages entirely,” Bischoff said.-from Bloomberg

BSE Ltd, Asia’s oldest stock exchange, is looking to launch its initial public offering (IPO) before the end of this calendar year to raise up to Rs.800 crore, according to two people aware of the development.

The exchange and the intermediaries it has hired are working on regulatory aspects of the IPO, and the draft share-sale prospectus is expected to be filed before the end of the April-June quarter, said one of the two persons, both of whom requested anonymity.

The size of the IPO is likely to be Rs.700-800 crore, said the second person.

BSE is looking at September or October to launch the public offer, said the first person.

“The exchange business is a very well-regulated space and therefore BSE has most of the regulation-related things in place, which will make work quicker,” he added.

Work on the IPO has been under way since January, when the BSE invited three or four merchant banks to initiate work on the share sale.

“BSE hopes to complete the formalities within 9 to 12 months. BSE has already appointed merchant bankers and lawyers for the purpose of preparing of documents including DRHP (draft red herring prospectus). Initial meetings have already been conducted amongst different participants for document preparation,” said a BSE spokesperson in response to an email from Mint seeking comment.

We had decided in January to allow stock exchanges to list. We have granted an in-principle approval to BSE to list,” said Sebi chairman U.K. Sinha.

The exchange is looking at a valuation of close to Rs.6,000 crore for the public share sale, said the second person quoted.

BSE counts foreign stock exchanges such as Deutsche Boerse AG and Singapore Exchange Ltd among its shareholders. Other investors include Life Insurance Corporation of India, State Bank of India and Bajaj Holdings and Investment Ltd. Foreign investors such as US billionaire George Soros’s hedge fund Quantum’s Mauritius investment arm Quantum (M) Ltd, Canada-based investor Thomas Caldwell’s Caldwell India Holdings Inc. and US fund Argonaut Private Equity are also investors in the exchange.-from Mint