Subscribe to get the latest posts sent to your email.

One reply on “Grasim: Disrupting Decorative Paints”

Is the De-rating of Asian Paints an Anomaly / Overreaction?

Market leader Asian Paints has seen its stock price reduce and trailing valuation multiple contract over the last few quarters, in spite of consistent earnings growth.

Specifically, the trailing p/e multiple which peaked at 103x Q3 FY22 TTM earnings of INR 32.12 on 20 January 2022 (the date of the Q3 FY22 earnings release), when the stock price was INR 3,306, shrunk to around 50x currently, basis Q3 FY24 TTM earnings. In other words, the valuation multiple has been reducing almost every quarter, even as the earnings have grown consistently over the last 24 months.

Apparently, the slowdown in volume growth in the decorative paints segment of Asian Paints is one of the reasons for the contraction of p/e multiple. Volume growth slowed down from 13% in 9 months to Q3 FY23, to 9% in 9 months to Q3 FY24.

Also, the markets seem to have turned jittery over the impending competition Asian Paints is likely to face from new entrants Grasim Industries and JSW Paints.

However, Asian Paints being the number 1 player, is well placed versus the competition.

To put things in perspective, the revenue, EBITDA and post-tax earnings of Asian Paints are larger than those of its three largest competitors combined. Also, the EBITDA margin of Asian Paints is superior to its competitors’. The 5-year CAGR for sales and post-tax profit for Asian Paints exceeds that of its key, large sized competitors, despite the fact that the former’s revenue size is larger than the competitors.

We view Asian Paints as the best proxy on India’s paints sector.

Threat from New Entrants

New entrants viz., Grasim Industries Ltd and JSW Paints Pvt Ltd are likely to become significant competitors to the incumbents over a period of time. It is feared that they might eventually try and eat into the market share of Asian Paints Ltd.

However, we believe the market has been overreacting to the threat of new competition, as Asian Paints being the number 1 player, is well placed to stave off the competition, old and new.

We believe it might be 2-3 years after the launch of Grasim Industries paints business, before Asian Paints begins to feel the heat from these two new competitors. Being the market leader, the management of Asian Paints Ltd will likely take all necessary steps to protect its turf, in the meantime.

Grasim Industries Ltd

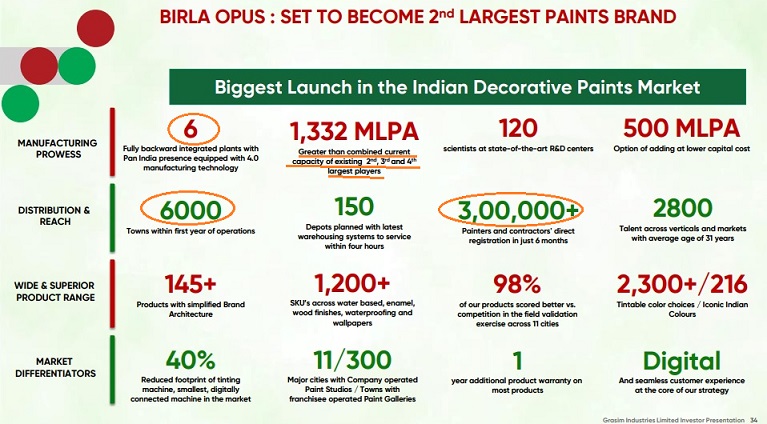

Grasim will set up six manufacturing plants in India by 2025, with a total capacity of 1,332 MLPA. This will make it the 2nd largest player by capacity in the Indian decorative paints sector. Grasim’s paints business has started trial production at plants at Ludhiana, Cheyyar and Panipat. The Q3 FY24 capex for its paints business was INR 1,088Cr. Cumulative capex for the paints business stood at INR 5,996 Cr till December 31, 2023, which is 59% of the planned outlay.

Its paints business will run under the ‘Birla Opus’ brand.

Two senior executives from its paints business participated in the Q3 FY24 concall of the company.

The company has an aggressive target to set up paints depots by the end of FY24. It has been signing agreements and leases and depots are operational to take in some of the trial production. Its objective is to have a pan-India national distribution by the end of FY24. The company will launch a full range of products under the Birla Opus paints brand in FY25. The brand will be launched in luxury, premium and economy categories, across multiple price points. The dealer onboarding has already commenced.

The company has stated its objective is to become the number two player in a reasonably short period of time and also turn profitable at the earliest possible.

PaintCraft, its painting services brand has been launched in 8 cities.

JSW Paints Pvt Ltd

JSW Paints Pvt Ltd, launched in 2019, reported a revenue of INR 1,616 Cr in FY23. The company aims to cross INR 2,000 Cr in revenue and expects to break even at the EBITDA level in FY24.

It has achieved a coverage of over 60% in paint-selling towns and increased its retailer network by adding more than 2,000 retailers every year. It has recently launched more than 20 new products across markets and will continue to launch new products.

Our View

While JSW Paints revenue of INR 1,616Cr is not negligible, it is a minuscule 5% of Asian Paints revenue of INR 34,488Cr in FY23. Since the launch of JSW Paints, the revenue growth at Asian Paints has not been impacted. JSW Paints might not make a significant dent in the market share of Asian Paints in the next 2-3 years.

Also, since JSW Paints has not been EBITDA positive at a scale of Rs 1,616Cr, it might indicate the use of the traditional strategy of offers, promotions and discounts to grow sales. Eventually, JSW Paints will face pressure to turn profitable, and as a result, will have to reduce offers and promotions. This might translate into lower margins for JSW Paints, going ahead.

To summarize

As regards the impending competition from Grasim Industries and JSW Paints, we would like to believe Asian Paints might have a head start of a couple of years before Grasim Industries is able to wean some market share away from it.

One reply on “Grasim: Disrupting Decorative Paints”

Is the De-rating of Asian Paints an Anomaly / Overreaction?

Market leader Asian Paints has seen its stock price reduce and trailing valuation multiple contract over the last few quarters, in spite of consistent earnings growth.

Specifically, the trailing p/e multiple which peaked at 103x Q3 FY22 TTM earnings of INR 32.12 on 20 January 2022 (the date of the Q3 FY22 earnings release), when the stock price was INR 3,306, shrunk to around 50x currently, basis Q3 FY24 TTM earnings. In other words, the valuation multiple has been reducing almost every quarter, even as the earnings have grown consistently over the last 24 months.

Apparently, the slowdown in volume growth in the decorative paints segment of Asian Paints is one of the reasons for the contraction of p/e multiple. Volume growth slowed down from 13% in 9 months to Q3 FY23, to 9% in 9 months to Q3 FY24.

Also, the markets seem to have turned jittery over the impending competition Asian Paints is likely to face from new entrants Grasim Industries and JSW Paints.

However, Asian Paints being the number 1 player, is well placed versus the competition.

To put things in perspective, the revenue, EBITDA and post-tax earnings of Asian Paints are larger than those of its three largest competitors combined. Also, the EBITDA margin of Asian Paints is superior to its competitors’. The 5-year CAGR for sales and post-tax profit for Asian Paints exceeds that of its key, large sized competitors, despite the fact that the former’s revenue size is larger than the competitors.

We view Asian Paints as the best proxy on India’s paints sector.

Threat from New Entrants

New entrants viz., Grasim Industries Ltd and JSW Paints Pvt Ltd are likely to become significant competitors to the incumbents over a period of time. It is feared that they might eventually try and eat into the market share of Asian Paints Ltd.

However, we believe the market has been overreacting to the threat of new competition, as Asian Paints being the number 1 player, is well placed to stave off the competition, old and new.

We believe it might be 2-3 years after the launch of Grasim Industries paints business, before Asian Paints begins to feel the heat from these two new competitors. Being the market leader, the management of Asian Paints Ltd will likely take all necessary steps to protect its turf, in the meantime.

Grasim Industries Ltd

Grasim will set up six manufacturing plants in India by 2025, with a total capacity of 1,332 MLPA. This will make it the 2nd largest player by capacity in the Indian decorative paints sector. Grasim’s paints business has started trial production at plants at Ludhiana, Cheyyar and Panipat. The Q3 FY24 capex for its paints business was INR 1,088Cr. Cumulative capex for the paints business stood at INR 5,996 Cr till December 31, 2023, which is 59% of the planned outlay.

Its paints business will run under the ‘Birla Opus’ brand.

Two senior executives from its paints business participated in the Q3 FY24 concall of the company.

The company has an aggressive target to set up paints depots by the end of FY24. It has been signing agreements and leases and depots are operational to take in some of the trial production. Its objective is to have a pan-India national distribution by the end of FY24. The company will launch a full range of products under the Birla Opus paints brand in FY25. The brand will be launched in luxury, premium and economy categories, across multiple price points. The dealer onboarding has already commenced.

The company has stated its objective is to become the number two player in a reasonably short period of time and also turn profitable at the earliest possible.

PaintCraft, its painting services brand has been launched in 8 cities.

JSW Paints Pvt Ltd

JSW Paints Pvt Ltd, launched in 2019, reported a revenue of INR 1,616 Cr in FY23. The company aims to cross INR 2,000 Cr in revenue and expects to break even at the EBITDA level in FY24.

It has achieved a coverage of over 60% in paint-selling towns and increased its retailer network by adding more than 2,000 retailers every year. It has recently launched more than 20 new products across markets and will continue to launch new products.

Our View

While JSW Paints revenue of INR 1,616Cr is not negligible, it is a minuscule 5% of Asian Paints revenue of INR 34,488Cr in FY23. Since the launch of JSW Paints, the revenue growth at Asian Paints has not been impacted. JSW Paints might not make a significant dent in the market share of Asian Paints in the next 2-3 years.

Also, since JSW Paints has not been EBITDA positive at a scale of Rs 1,616Cr, it might indicate the use of the traditional strategy of offers, promotions and discounts to grow sales. Eventually, JSW Paints will face pressure to turn profitable, and as a result, will have to reduce offers and promotions. This might translate into lower margins for JSW Paints, going ahead.

To summarize

As regards the impending competition from Grasim Industries and JSW Paints, we would like to believe Asian Paints might have a head start of a couple of years before Grasim Industries is able to wean some market share away from it.