Categories Excerpts Good Times Vs Hard Times Post author By Raoji Post date September 10, 2025 No Comments on Good Times Vs Hard Times Source: Jason Zweig, Wall Street Journal Share this: Share on Facebook (Opens in new window) Facebook Share on LinkedIn (Opens in new window) LinkedIn Share on X (Opens in new window) X Share on WhatsApp (Opens in new window) WhatsApp Email a link to a friend (Opens in new window) Email

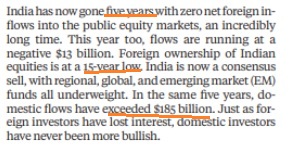

Categories Excerpts Desis Vs Goras Post author By Raoji Post date August 26, 2025 No Comments on Desis Vs Goras Source: Akash Prakash, Business Standard Share this: Share on Facebook (Opens in new window) Facebook Share on LinkedIn (Opens in new window) LinkedIn Share on X (Opens in new window) X Share on WhatsApp (Opens in new window) WhatsApp Email a link to a friend (Opens in new window) Email

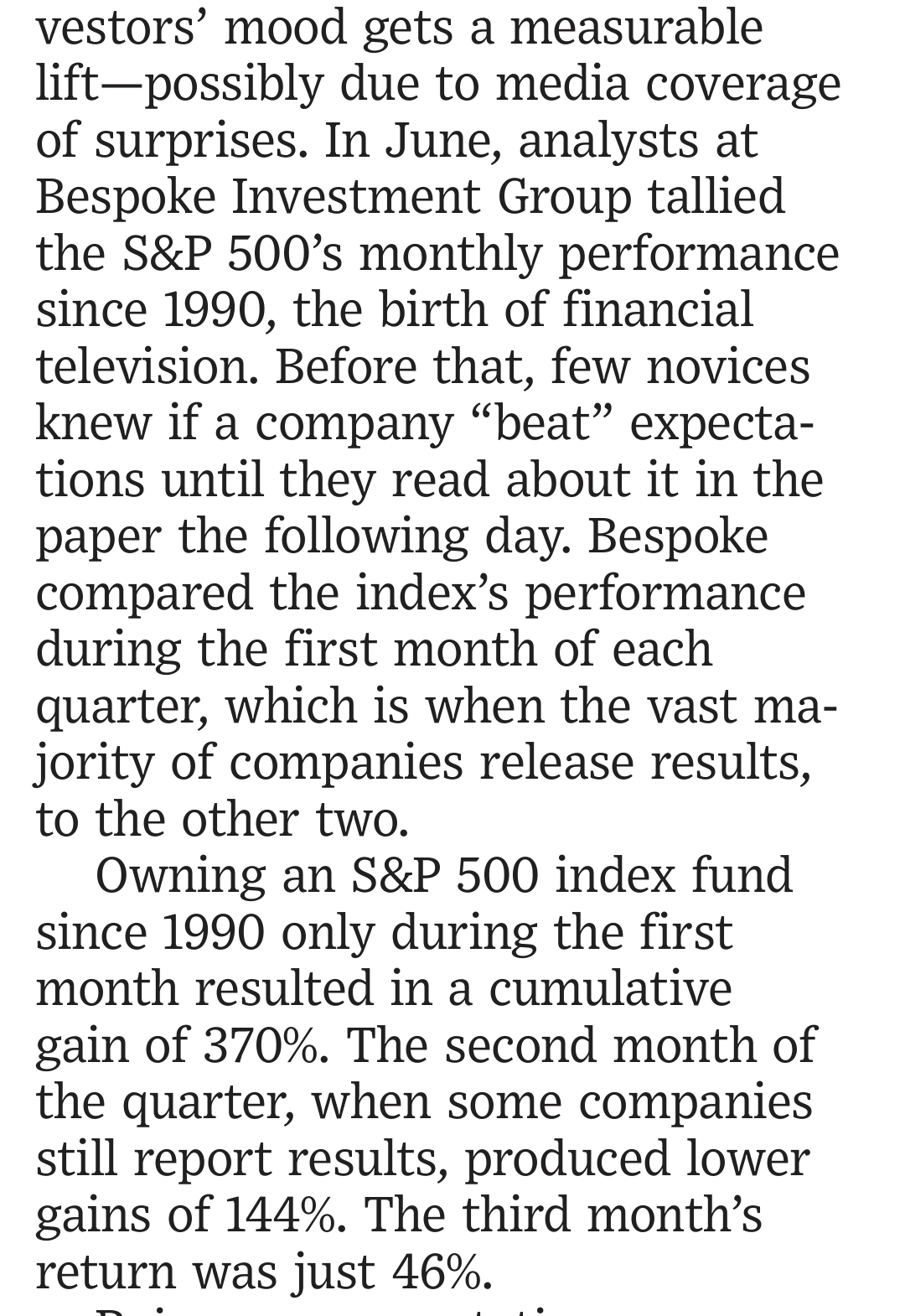

Categories Excerpts When to buy an Index Fund Post author By Raoji Post date July 16, 2025 No Comments on When to buy an Index Fund Source : Wall Street Journal Share this: Share on Facebook (Opens in new window) Facebook Share on LinkedIn (Opens in new window) LinkedIn Share on X (Opens in new window) X Share on WhatsApp (Opens in new window) WhatsApp Email a link to a friend (Opens in new window) Email

Categories Excerpts 5 Risks in Global Markets Post author By Raoji Post date July 3, 2025 No Comments on 5 Risks in Global Markets Source : Satyajit Das, Financial Times Share this: Share on Facebook (Opens in new window) Facebook Share on LinkedIn (Opens in new window) LinkedIn Share on X (Opens in new window) X Share on WhatsApp (Opens in new window) WhatsApp Email a link to a friend (Opens in new window) Email

Categories Excerpts The $ 1,000 Trump Account Post author By Raoji Post date May 26, 2025 No Comments on The $ 1,000 Trump Account Source: Financial Times Share this: Share on Facebook (Opens in new window) Facebook Share on LinkedIn (Opens in new window) LinkedIn Share on X (Opens in new window) X Share on WhatsApp (Opens in new window) WhatsApp Email a link to a friend (Opens in new window) Email