Subscribe to get the latest posts sent to your email.

One reply on “ITC | Price changes Perception”

Agree!

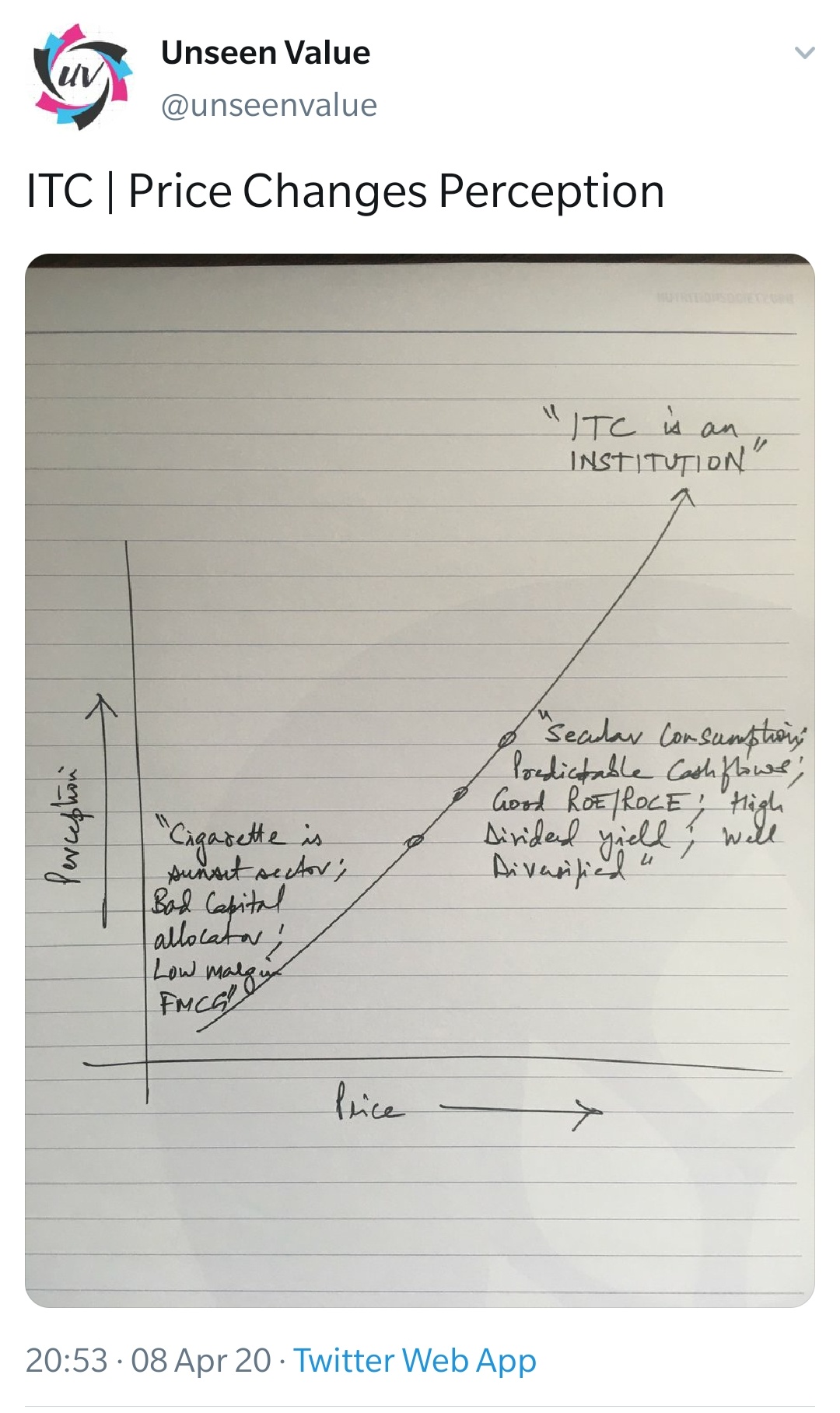

There are few WRONG PERCEPTION about the ITC and my view about it.

No promoters:

I believe, people should ignore this as this company consistently able to increase its “Net profit” over few decades, it MEANS the MANAGEMENT is GOOD and there is WELL ESTABLISHED SUCCESSFUL ORGANOGRAM. If the promoter holdings is high, the BOARD consist of only family members or preferred people, which is WRONG. NEED of diversed people for a good administration and bring necessary changes.

Cigarette is slowing/decreasing business:

I have never heard any negative comments about other tobacco company. I don’t know why people are so obsessed only with ITC. India’s population is expected to grow much higher, even if some % of tobacco user’s will be reduced, still large number of population are consumers. It means, number of people who use tobacco will continue to maintain as such.

Huge taxation on cigarette business:

This won’t affect sales, as people will never limit expenses on their entertainment and relaxation. Since cigarette usage is kind of addiction, people will continue to buy the product despite of any price. BRAND ATTACHMENT also contribute SIGNIFICANTLY.

A huge taxation lead to increased price, therefore people will try to find an alternative which is available in the black market. As we are in the globalization era, finding illegally imported tobacco product is NOT a big problem. Therefore, GOVT CAN’T INCREASE TAX BEYOND CERTAIN POINT, AS THAT WILL REDUCE THE SALES OF LEGALISED PRODUCT, OBVIOUSLY LESS TAX COLLECTION TO THE GOVT.

HIGH dividend payout policy, as per the recent announcement:

People are concerning that a “high payout” ratio may lead to cash crunch it means difficult to invest in new business or avenues. ITC’s net profit in 2019 is 12,592crores and it is consistently increased. Even if they pay out 85% to its shareholders, still it will have around 2, 000 crore every annum. In the last 10 years, the net profit increased from 3325 to 12596 crores, so every year they will retain huge money. So higher dividend payout ratio WON’T LEAD TO CASH CRUNCH. Also, tobacco and FMCG business won’t require “HEFTY RECURRING EXPENDITURE”, once the production units are established.

Concern:

Since there is promoter holdings which usually constitute major shares holdings, there are crores of shares freely available in the market. I guess, this have been contribute hugely for price fluctuation/reduction.

Note: I am a shareholder and will increase once the current economic and corona chaos is controlled.

One reply on “ITC | Price changes Perception”

Agree!

There are few WRONG PERCEPTION about the ITC and my view about it.

No promoters:

I believe, people should ignore this as this company consistently able to increase its “Net profit” over few decades, it MEANS the MANAGEMENT is GOOD and there is WELL ESTABLISHED SUCCESSFUL ORGANOGRAM. If the promoter holdings is high, the BOARD consist of only family members or preferred people, which is WRONG. NEED of diversed people for a good administration and bring necessary changes.

Cigarette is slowing/decreasing business:

I have never heard any negative comments about other tobacco company. I don’t know why people are so obsessed only with ITC. India’s population is expected to grow much higher, even if some % of tobacco user’s will be reduced, still large number of population are consumers. It means, number of people who use tobacco will continue to maintain as such.

Huge taxation on cigarette business:

This won’t affect sales, as people will never limit expenses on their entertainment and relaxation. Since cigarette usage is kind of addiction, people will continue to buy the product despite of any price. BRAND ATTACHMENT also contribute SIGNIFICANTLY.

A huge taxation lead to increased price, therefore people will try to find an alternative which is available in the black market. As we are in the globalization era, finding illegally imported tobacco product is NOT a big problem. Therefore, GOVT CAN’T INCREASE TAX BEYOND CERTAIN POINT, AS THAT WILL REDUCE THE SALES OF LEGALISED PRODUCT, OBVIOUSLY LESS TAX COLLECTION TO THE GOVT.

HIGH dividend payout policy, as per the recent announcement:

People are concerning that a “high payout” ratio may lead to cash crunch it means difficult to invest in new business or avenues. ITC’s net profit in 2019 is 12,592crores and it is consistently increased. Even if they pay out 85% to its shareholders, still it will have around 2, 000 crore every annum. In the last 10 years, the net profit increased from 3325 to 12596 crores, so every year they will retain huge money. So higher dividend payout ratio WON’T LEAD TO CASH CRUNCH. Also, tobacco and FMCG business won’t require “HEFTY RECURRING EXPENDITURE”, once the production units are established.

Concern:

Since there is promoter holdings which usually constitute major shares holdings, there are crores of shares freely available in the market. I guess, this have been contribute hugely for price fluctuation/reduction.

Note: I am a shareholder and will increase once the current economic and corona chaos is controlled.