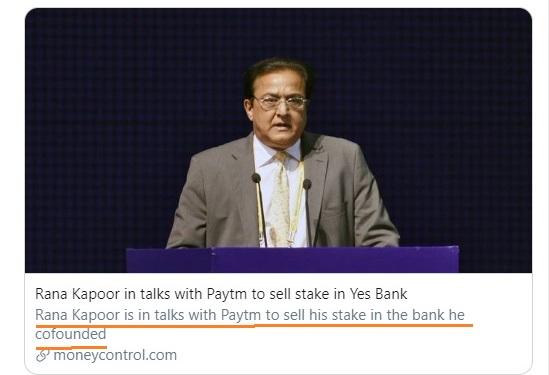

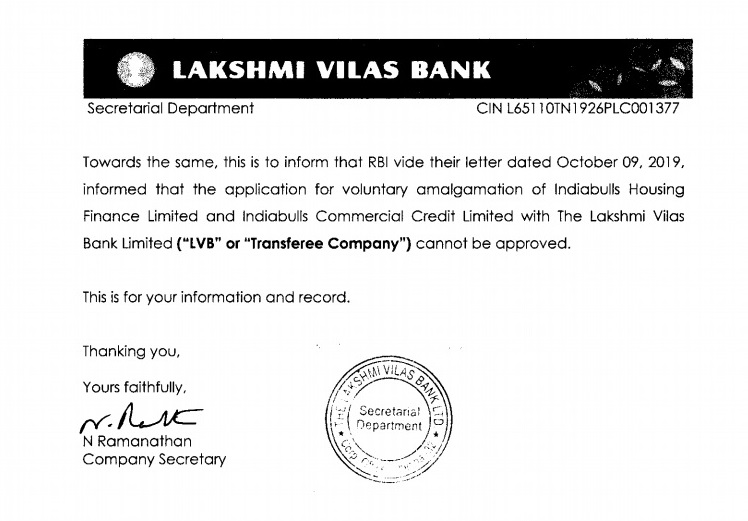

Hat Tip: Divyeshbhai

Hat Tip: Divyeshbhai

How dare a Credit Agency downgrade a Co’s ratings when it has been pre-emptively fired?

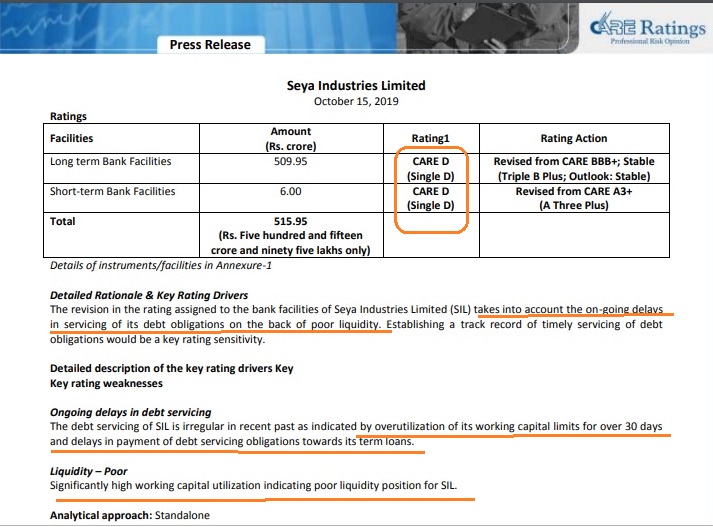

Today Care Ratings downgraded Seya Industries

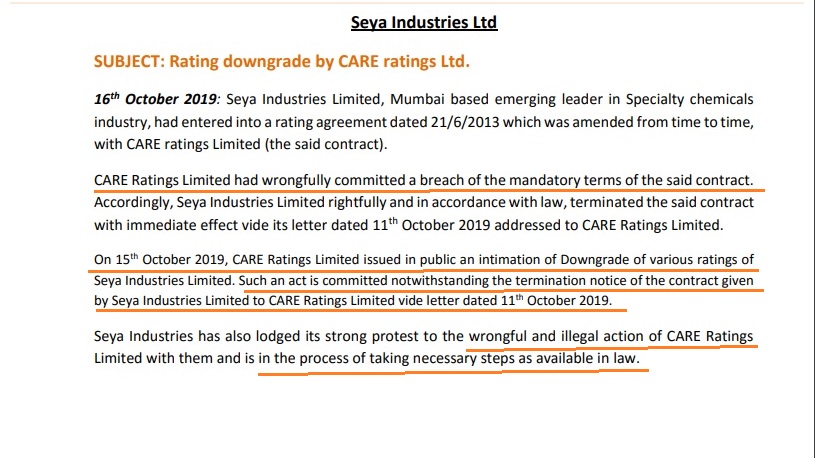

Seya Industries , not only did not inform the exchanges on 15th Oct about the downgrade but instead gave a blustering response.

Buy

Reject

Dhoka?

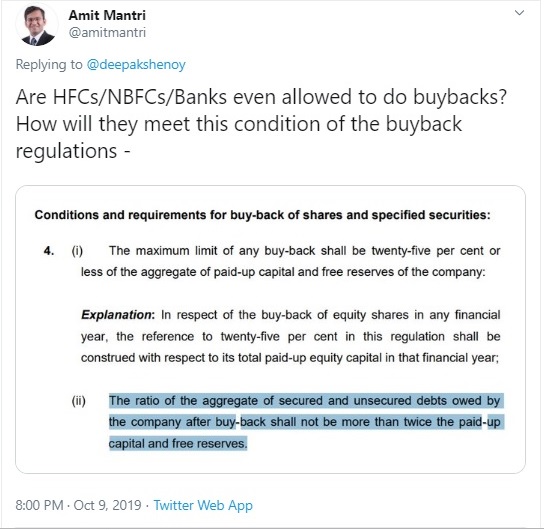

Hat Tip: Divyeshbhai

One Year Back:

Now: