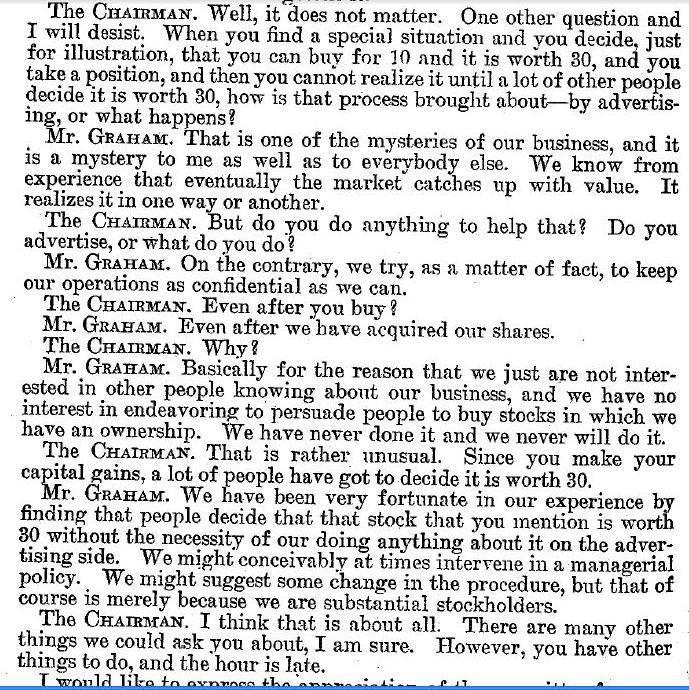

-from Ben Graham’s testimony to the US Senate Committee on Banking & Currency on March,1955

-from Ben Graham’s testimony to the US Senate Committee on Banking & Currency on March,1955

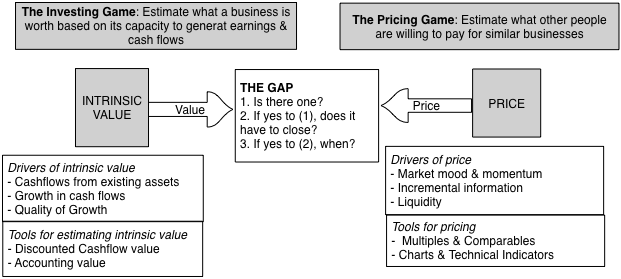

Source:Samir Arora

You can value an asset, based upon its fundamentals (cash flows, growth and risk) or price it, based upon what others are paying for similar assets, and the two can yield different numbers.

In public investing, I have argued that this plays out in whether you choose to play the value game (invest in assets where the price < value and hope that the market corrects) or the pricing game (where you trade assets, buying at a lower price and hoping to sell at a higher).

–wrote Aswath Damodaran

The Securities Exchange Board of India (Sebi) went on an alert on Thursday after a major crash in domestic stocks and the currency amid rising hostilities across the border.

The market regulator has sought a report from domestic stock exchanges on their preparedness to deal with any eventuality in the wake of a sharp plunge in the benchmark equity indices following Indian Army’s surgical strikes on terror bases in Pakistan-occupied Kashmir (POK).

The benchmark Sensex lost 465 points while the Nifty50 crashed 154 points in knee-jerk response to the signs of rising hostilities between the two neighbours.

The rupee weakened to a one-week low of 66.91, marking the worst fall for the domestic currency since the Brexit vote in June. The domestic currency, though, recovered a bit to settle at 66.85, down 39 paise over previous day closing of 66.46.

According to reports, the market regulator has asked the stock exchanges to draft contingency plans and submit detailed reports to it by this evening.

The India VIX shot up by 33 percentage points to 18.45, which was the biggest rise in seven years.

The 10-year bond yield jumped to a one-year high. Fresh reports suggested that villages in Punjab, 10 km from international border with Pakistan, are being evacuated.

DGMO Lt Gen Ranbir Singh on Thursday said India carried out surgical strikes in Pakistan-occupied Kashmir, inflicting heavy casualties on terrorists and those protecting them.

Following the press briefing by DGMO, the domestic equity indices plunged up to 4 per cent amid concerns that foreign investors, who have pumped in about Rs 50,000 crore into domestic stocks so far this year, may run for the exit door should the tensions rise further.

Buffett has often said, “I could improve your ultimate financial welfare by giving you a ticket with only twenty slots in it so that you had twenty punches – representing all the investments that you got to make in a lifetime. And once you’d punched through the card, you couldn’t make any more investments at all. Under those rules, you’d really think carefully about what you did, and you’d be forced to load up on what you’d really thought about. So you’d do so much better.”