frm Consolidated AR from Reserves I found following

Exchange Fluctuation reserve

-1143.377

-830.955

-583.898

-359.471

-210.29

-141.926 which is abt 3100 crs

Now also see PL frm 2010

Profit & Loss Account Balance

2320.892

1671.018

2699.598

2266.948

1764.014

1339.912

1420.5673

– which is 13000 crs ???

very interesting !!!!! sharp eye

Am i right?

A. Currency Translation Reserve in crs (change from previous year)

2016: 313

2015: 247

2014:229

2012:149

2012:69

Total: 1002

B. Retained earnings in crores (change from previous year)

2015: 665

2015: 403

2014: 443

2013: 502

2012:365

Total: 2378

Total: (A+B): 1072+2378=3450

C. Net Profit in Crs

2016: 701

2015: 475

2014: 545

2013: 623

2012:464

2011: 457

Total: 3265

still a difference of 185 crores though.

From a Motilal Oswal report:

Net worth under IFRS declines on migration to IGAAP

* INR6.4b writes down in value of assets while transiting from IGAAP to IFRS in FY11

* In FY11, the company, under the option given by the SEBI, voluntarily adopted the IFRS reporting standards.

*Upon migration, as permitted, the company recognized assets (some of which were revalued at fair market value) and liabilities based on first-time adoption principles of IFRS and adjusted the net decline in the value of assets (~INR6.4b) against the reserves

*The company also voluntarily presented consolidated figures under IFRS for FY16.

* On account of this move, as at 2QFY16, management in the concall highlighted the following:

-Intangible assets reduced by INR3.8b as IGAAP does not allow indefinite life and amortization that were due in the intervening period from FY11 to FY15.

– Deferred tax asset reduced by INR3.9b.

– Intangible assets lowered by INR3.4b. This was on account of revaluation of tangible assets, which was done on the basis of fair value derived at the transition from IGAAP to IFRS. Fair value of these assets was available for the organization for including in revaluation reserves.

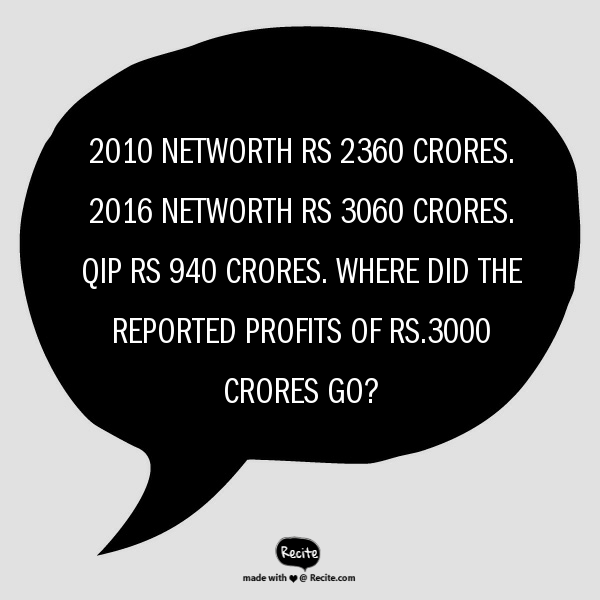

* Over FY11-FY16, we note that the company had IGAAP net worth of INR23.6b, which just increased to INR30.6b despite raising INR9.4b by dilution of equity

3 replies on “The Glenmark Mystery”

frm Consolidated AR from Reserves I found following

Exchange Fluctuation reserve

-1143.377

-830.955

-583.898

-359.471

-210.29

-141.926 which is abt 3100 crs

Now also see PL frm 2010

Profit & Loss Account Balance

2320.892

1671.018

2699.598

2266.948

1764.014

1339.912

1420.5673

– which is 13000 crs ???

very interesting !!!!! sharp eye

Am i right?

A. Currency Translation Reserve in crs (change from previous year)

2016: 313

2015: 247

2014:229

2012:149

2012:69

Total: 1002

B. Retained earnings in crores (change from previous year)

2015: 665

2015: 403

2014: 443

2013: 502

2012:365

Total: 2378

Total: (A+B): 1072+2378=3450

C. Net Profit in Crs

2016: 701

2015: 475

2014: 545

2013: 623

2012:464

2011: 457

Total: 3265

still a difference of 185 crores though.

From a Motilal Oswal report:

Net worth under IFRS declines on migration to IGAAP

* INR6.4b writes down in value of assets while transiting from IGAAP to IFRS in FY11

* In FY11, the company, under the option given by the SEBI, voluntarily adopted the IFRS reporting standards.

*Upon migration, as permitted, the company recognized assets (some of which were revalued at fair market value) and liabilities based on first-time adoption principles of IFRS and adjusted the net decline in the value of assets (~INR6.4b) against the reserves

*The company also voluntarily presented consolidated figures under IFRS for FY16.

* On account of this move, as at 2QFY16, management in the concall highlighted the following:

-Intangible assets reduced by INR3.8b as IGAAP does not allow indefinite life and amortization that were due in the intervening period from FY11 to FY15.

– Deferred tax asset reduced by INR3.9b.

– Intangible assets lowered by INR3.4b. This was on account of revaluation of tangible assets, which was done on the basis of fair value derived at the transition from IGAAP to IFRS. Fair value of these assets was available for the organization for including in revaluation reserves.

* Over FY11-FY16, we note that the company had IGAAP net worth of INR23.6b, which just increased to INR30.6b despite raising INR9.4b by dilution of equity